08 - Improving Variational Quantum Optimization using CVaR

[1]:

# This code is from the tutorial at:

# https://qiskit-community.github.io/qiskit-optimization/tutorials/08_cvar_optimization.html

[2]:

from qiskit.circuit.library import RealAmplitudes

from qiskit_algorithms.optimizers import COBYLA

from qiskit_algorithms import NumPyMinimumEigensolver, SamplingVQE

from qiskit_algorithms.utils import algorithm_globals

# Switch to Quantum Rings's Sampler

#from qiskit.primitives import Sampler

from quantumrings.toolkit.qiskit import QrSamplerV1 as Sampler

from qiskit_optimization.converters import LinearEqualityToPenalty

from qiskit_optimization.algorithms import MinimumEigenOptimizer

from qiskit_optimization.translators import from_docplex_mp

import numpy as np

import matplotlib.pyplot as plt

from docplex.mp.model import Model

[3]:

algorithm_globals.random_seed = 123456

[4]:

# prepare problem instance

n = 6 # number of assets

q = 0.5 # risk factor

budget = n // 2 # budget

penalty = 2 * n # scaling of penalty term

[5]:

# instance from [1]

mu = np.array([0.7313, 0.9893, 0.2725, 0.8750, 0.7667, 0.3622])

sigma = np.array(

[

[0.7312, -0.6233, 0.4689, -0.5452, -0.0082, -0.3809],

[-0.6233, 2.4732, -0.7538, 2.4659, -0.0733, 0.8945],

[0.4689, -0.7538, 1.1543, -1.4095, 0.0007, -0.4301],

[-0.5452, 2.4659, -1.4095, 3.5067, 0.2012, 1.0922],

[-0.0082, -0.0733, 0.0007, 0.2012, 0.6231, 0.1509],

[-0.3809, 0.8945, -0.4301, 1.0922, 0.1509, 0.8992],

]

)

# or create random instance

# mu, sigma = portfolio.random_model(n, seed=123) # expected returns and covariance matrix

[6]:

# create docplex model

mdl = Model("portfolio_optimization")

x = mdl.binary_var_list(range(n), name="x")

objective = mdl.sum([mu[i] * x[i] for i in range(n)])

objective -= q * mdl.sum([sigma[i, j] * x[i] * x[j] for i in range(n) for j in range(n)])

mdl.maximize(objective)

mdl.add_constraint(mdl.sum(x[i] for i in range(n)) == budget)

# case to

qp = from_docplex_mp(mdl)

[7]:

# solve classically as reference

opt_result = MinimumEigenOptimizer(NumPyMinimumEigensolver()).solve(qp)

print(opt_result.prettyprint())

objective function value: 1.27835

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

[8]:

# we convert the problem to an unconstrained problem for further analysis,

# otherwise this would not be necessary as the MinimumEigenSolver would do this

# translation automatically

linear2penalty = LinearEqualityToPenalty(penalty=penalty)

qp = linear2penalty.convert(qp)

_, offset = qp.to_ising()

Minimum Eigen Optimizer using SamplingVQE

[9]:

# set classical optimizer

maxiter = 100

optimizer = COBYLA(maxiter=maxiter)

# set variational ansatz

ansatz = RealAmplitudes(n, reps=1)

m = ansatz.num_parameters

# set sampler

sampler = Sampler()

# run variational optimization for different values of alpha

alphas = [1.0, 0.50, 0.25] # confidence levels to be evaluated

[10]:

# dictionaries to store optimization progress and results

objectives = {alpha: [] for alpha in alphas} # set of tested objective functions w.r.t. alpha

results = {} # results of minimum eigensolver w.r.t alpha

# callback to store intermediate results

def callback(i, params, obj, stddev, alpha):

# we translate the objective from the internal Ising representation

# to the original optimization problem

objectives[alpha].append(np.real_if_close(-(obj + offset)))

# loop over all given alpha values

for alpha in alphas:

# initialize SamplingVQE using CVaR

vqe = SamplingVQE(

sampler=sampler,

ansatz=ansatz,

optimizer=optimizer,

aggregation=alpha,

callback=lambda i, params, obj, stddev: callback(i, params, obj, stddev, alpha),

)

# initialize optimization algorithm based on CVaR-SamplingVQE

opt_alg = MinimumEigenOptimizer(vqe)

# solve problem

results[alpha] = opt_alg.solve(qp)

print(f"Count of raw samples: {len(results[alpha].raw_samples)}")

print(f"Count of samples: {len(results[alpha].samples)}")

print(type(results[alpha].min_eigen_solver_result))

print(f"Count of eigenstate binary probs: {len(results[alpha].min_eigen_solver_result.eigenstate.binary_probabilities().values())}")

# print results

print("alpha = {}:".format(alpha))

print(results[alpha].prettyprint())

print()

Count of raw samples: 26

Count of samples: 26

<class 'qiskit_algorithms.minimum_eigensolvers.sampling_vqe.SamplingVQEResult'>

Count of eigenstate binary probs: 26

alpha = 1.0:

objective function value: 0.9716499999999968

variable values: x_0=1.0, x_1=0.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=1.0

status: SUCCESS

Count of raw samples: 25

Count of samples: 25

<class 'qiskit_algorithms.minimum_eigensolvers.sampling_vqe.SamplingVQEResult'>

Count of eigenstate binary probs: 25

alpha = 0.5:

objective function value: 0.7296000000000049

variable values: x_0=0.0, x_1=1.0, x_2=1.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

Count of raw samples: 50

Count of samples: 50

<class 'qiskit_algorithms.minimum_eigensolvers.sampling_vqe.SamplingVQEResult'>

Count of eigenstate binary probs: 50

alpha = 0.25:

objective function value: 1.2783500000000174

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

[11]:

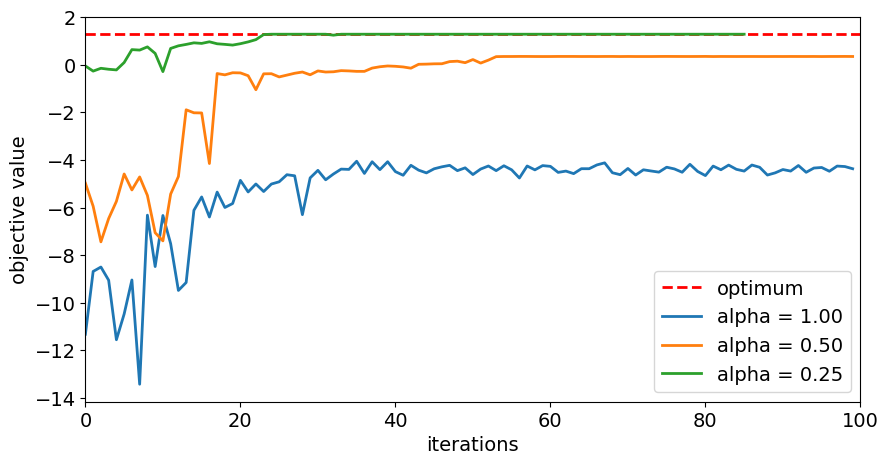

# plot resulting history of objective values

plt.figure(figsize=(10, 5))

plt.plot([0, maxiter], [opt_result.fval, opt_result.fval], "r--", linewidth=2, label="optimum")

for alpha in alphas:

plt.plot(objectives[alpha], label="alpha = %.2f" % alpha, linewidth=2)

plt.legend(loc="lower right", fontsize=14)

plt.xlim(0, maxiter)

plt.xticks(fontsize=14)

plt.xlabel("iterations", fontsize=14)

plt.yticks(fontsize=14)

plt.ylabel("objective value", fontsize=14)

plt.show()

[12]:

# evaluate and sort all objective values

objective_values = np.zeros(2**n)

for i in range(2**n):

x_bin = ("{0:0%sb}" % n).format(i)

x = [0 if x_ == "0" else 1 for x_ in reversed(x_bin)]

objective_values[i] = qp.objective.evaluate(x)

ind = np.argsort(objective_values)

# evaluate final optimal probability for each alpha

for alpha in alphas:

probabilities = np.fromiter(

results[alpha].min_eigen_solver_result.eigenstate.binary_probabilities().values(),

dtype=float,

)

# Fix, because, zero or close to zero states may not be present in the binary_probabilities

# causing a mismatch with the number of items in ind.

if ( len(probabilities) < len(ind)):

probabilities = np.append(probabilities, [0] * (len(ind) - len(probabilities)))

print("optimal probability (alpha = %.2f): %.4f" % (alpha, probabilities[ind][-1:]))

optimal probability (alpha = 1.00): 0.0020

optimal probability (alpha = 0.50): 0.0098

optimal probability (alpha = 0.25): 0.0273

C:\Users\vkasi\AppData\Local\Temp\ipykernel_33812\2091013010.py:22: DeprecationWarning: Conversion of an array with ndim > 0 to a scalar is deprecated, and will error in future. Ensure you extract a single element from your array before performing this operation. (Deprecated NumPy 1.25.)

print("optimal probability (alpha = %.2f): %.4f" % (alpha, probabilities[ind][-1:]))

[ ]: