07-Finance Tutorial-Pricing Asian Barrier Spreads

[ ]:

#this example is at:

# https://qiskit-community.github.io/qiskit-finance/tutorials/07_asian_barrier_spread_pricing.html

[1]:

import matplotlib.pyplot as plt

from scipy.interpolate import griddata

%matplotlib inline

import numpy as np

from qiskit import QuantumRegister, QuantumCircuit, AncillaRegister, transpile

from qiskit.circuit.library import IntegerComparator, WeightedAdder, LinearAmplitudeFunction

from qiskit_algorithms import IterativeAmplitudeEstimation, EstimationProblem

#from qiskit_aer.primitives import Sampler

from qiskit_finance.circuit.library import LogNormalDistribution

from quantumrings.toolkit.qiskit import QrSamplerV1 as Sampler

[2]:

# number of qubits per dimension to represent the uncertainty

num_uncertainty_qubits = 2

# parameters for considered random distribution

S = 2.0 # initial spot price

vol = 0.4 # volatility of 40%

r = 0.05 # annual interest rate of 4%

T = 40 / 365 # 40 days to maturity

# resulting parameters for log-normal distribution

mu = (r - 0.5 * vol**2) * T + np.log(S)

sigma = vol * np.sqrt(T)

mean = np.exp(mu + sigma**2 / 2)

variance = (np.exp(sigma**2) - 1) * np.exp(2 * mu + sigma**2)

stddev = np.sqrt(variance)

# lowest and highest value considered for the spot price; in between, an equidistant discretization is considered.

low = np.maximum(0, mean - 3 * stddev)

high = mean + 3 * stddev

# map to higher dimensional distribution

# for simplicity assuming dimensions are independent and identically distributed)

dimension = 2

num_qubits = [num_uncertainty_qubits] * dimension

low = low * np.ones(dimension)

high = high * np.ones(dimension)

mu = mu * np.ones(dimension)

cov = sigma**2 * np.eye(dimension)

# construct circuit

u = LogNormalDistribution(num_qubits=num_qubits, mu=mu, sigma=cov, bounds=(list(zip(low, high))))

[3]:

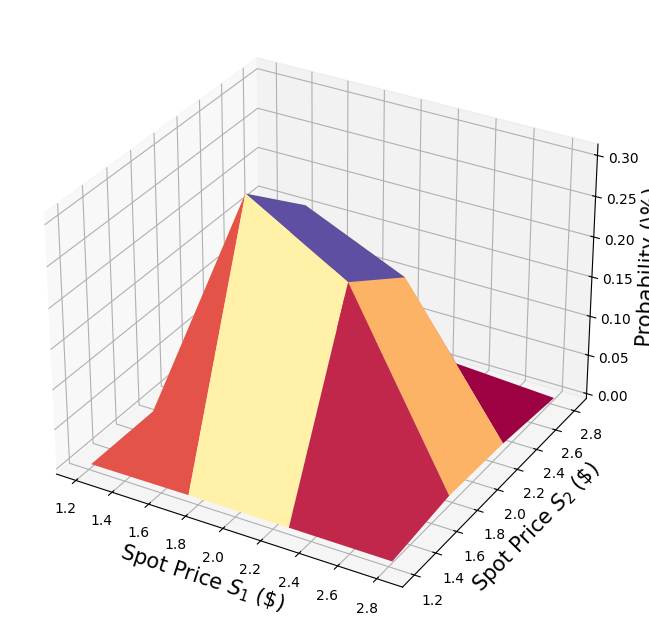

# plot PDF of uncertainty model

x = [v[0] for v in u.values]

y = [v[1] for v in u.values]

z = u.probabilities

# z = map(float, z)

# z = list(map(float, z))

resolution = np.array([2**n for n in num_qubits]) * 1j

grid_x, grid_y = np.mgrid[min(x) : max(x) : resolution[0], min(y) : max(y) : resolution[1]]

grid_z = griddata((x, y), z, (grid_x, grid_y))

plt.figure(figsize=(10, 8))

ax = plt.axes(projection="3d")

ax.plot_surface(grid_x, grid_y, grid_z, cmap=plt.cm.Spectral)

ax.set_xlabel("Spot Price $S_1$ (\$)", size=15)

ax.set_ylabel("Spot Price $S_2$ (\$)", size=15)

ax.set_zlabel("Probability (\%)", size=15)

plt.show()

[4]:

# determine number of qubits required to represent total loss

weights = []

for n in num_qubits:

for i in range(n):

weights += [2**i]

# create aggregation circuit

agg = WeightedAdder(sum(num_qubits), weights)

n_s = agg.num_sum_qubits

n_aux = agg.num_qubits - n_s - agg.num_state_qubits # number of additional qubits

[5]:

# set the strike price (should be within the low and the high value of the uncertainty)

strike_price_1 = 3

strike_price_2 = 4

# set the barrier threshold

barrier = 2.5

# map strike prices and barrier threshold from [low, high] to {0, ..., 2^n-1}

max_value = 2**n_s - 1

low_ = low[0]

high_ = high[0]

mapped_strike_price_1 = (

(strike_price_1 - dimension * low_) / (high_ - low_) * (2**num_uncertainty_qubits - 1)

)

mapped_strike_price_2 = (

(strike_price_2 - dimension * low_) / (high_ - low_) * (2**num_uncertainty_qubits - 1)

)

mapped_barrier = (barrier - low) / (high - low) * (2**num_uncertainty_qubits - 1)

[6]:

# condition and condition result

conditions = []

barrier_thresholds = [2] * dimension

n_aux_conditions = 0

for i in range(dimension):

# target dimension of random distribution and corresponding condition (which is required to be True)

comparator = IntegerComparator(num_qubits[i], mapped_barrier[i] + 1, geq=False)

n_aux_conditions = max(n_aux_conditions, comparator.num_ancillas)

conditions += [comparator]

[7]:

# set the approximation scaling for the payoff function

c_approx = 0.25

# setup piecewise linear objective fcuntion

breakpoints = [0, mapped_strike_price_1, mapped_strike_price_2]

slopes = [0, 1, 0]

offsets = [0, 0, mapped_strike_price_2 - mapped_strike_price_1]

f_min = 0

f_max = mapped_strike_price_2 - mapped_strike_price_1

objective = LinearAmplitudeFunction(

n_s,

slopes,

offsets,

domain=(0, max_value),

image=(f_min, f_max),

rescaling_factor=c_approx,

breakpoints=breakpoints,

)

[8]:

# number of qubits per dimension to represent the uncertainty

num_uncertainty_qubits = 2

# parameters for considered random distribution

S = 2.0 # initial spot price

vol = 0.4 # volatility of 40%

r = 0.05 # annual interest rate of 4%

T = 40 / 365 # 40 days to maturity

# resulting parameters for log-normal distribution

mu = (r - 0.5 * vol**2) * T + np.log(S)

sigma = vol * np.sqrt(T)

mean = np.exp(mu + sigma**2 / 2)

variance = (np.exp(sigma**2) - 1) * np.exp(2 * mu + sigma**2)

stddev = np.sqrt(variance)

# lowest and highest value considered for the spot price; in between, an equidistant discretization is considered.

low = np.maximum(0, mean - 3 * stddev)

high = mean + 3 * stddev

# map to higher dimensional distribution

# for simplicity assuming dimensions are independent and identically distributed)

dimension = 2

num_qubits = [num_uncertainty_qubits] * dimension

low = low * np.ones(dimension)

high = high * np.ones(dimension)

mu = mu * np.ones(dimension)

cov = sigma**2 * np.eye(dimension)

# construct circuit

u = LogNormalDistribution(num_qubits=num_qubits, mu=mu, sigma=cov, bounds=list(zip(low, high)))

[9]:

# define overall multivariate problem

qr_state = QuantumRegister(u.num_qubits, "state") # to load the probability distribution

qr_obj = QuantumRegister(1, "obj") # to encode the function values

ar_sum = AncillaRegister(n_s, "sum") # number of qubits used to encode the sum

ar_cond = AncillaRegister(len(conditions) + 1, "conditions")

ar = AncillaRegister(

max(n_aux, n_aux_conditions, objective.num_ancillas), "work"

) # additional qubits

objective_index = u.num_qubits

# define the circuit

asian_barrier_spread = QuantumCircuit(qr_state, qr_obj, ar_cond, ar_sum, ar)

# load the probability distribution

asian_barrier_spread.append(u, qr_state)

# apply the conditions

for i, cond in enumerate(conditions):

state_qubits = qr_state[(num_uncertainty_qubits * i) : (num_uncertainty_qubits * (i + 1))]

asian_barrier_spread.append(cond, state_qubits + [ar_cond[i]] + ar[: cond.num_ancillas])

# aggregate the conditions on a single qubit

asian_barrier_spread.mcx(ar_cond[:-1], ar_cond[-1])

# apply the aggregation function controlled on the condition

asian_barrier_spread.append(agg.control(), [ar_cond[-1]] + qr_state[:] + ar_sum[:] + ar[:n_aux])

# apply the payoff function

asian_barrier_spread.append(objective, ar_sum[:] + qr_obj[:] + ar[: objective.num_ancillas])

# uncompute the aggregation

asian_barrier_spread.append(

agg.inverse().control(), [ar_cond[-1]] + qr_state[:] + ar_sum[:] + ar[:n_aux]

)

# uncompute the conditions

asian_barrier_spread.mcx(ar_cond[:-1], ar_cond[-1])

for j, cond in enumerate(reversed(conditions)):

i = len(conditions) - j - 1

state_qubits = qr_state[(num_uncertainty_qubits * i) : (num_uncertainty_qubits * (i + 1))]

asian_barrier_spread.append(

cond.inverse(), state_qubits + [ar_cond[i]] + ar[: cond.num_ancillas]

)

print(asian_barrier_spread.draw())

print("objective qubit index", objective_index)

┌───────┐┌──────┐ ┌───────────┐ ┌──────────────┐»

state_0: ┤0 ├┤0 ├─────────────┤1 ├──────┤1 ├»

│ ││ │ │ │ │ │»

state_1: ┤1 ├┤1 ├─────────────┤2 ├──────┤2 ├»

│ P(X) ││ │┌──────┐ │ │ │ │»

state_2: ┤2 ├┤ ├┤0 ├─────┤3 ├──────┤3 ├»

│ ││ ││ │ │ │ │ │»

state_3: ┤3 ├┤ ├┤1 ├─────┤4 ├──────┤4 ├»

└───────┘│ ││ │ │ │┌────┐│ │»

obj: ─────────┤ ├┤ ├─────┤ ├┤3 ├┤ ├»

│ ││ │ │ ││ ││ │»

conditions_0: ─────────┤2 ├┤ ├──■──┤ ├┤ ├┤ ├»

│ cmp ││ │ │ │ ││ ││ │»

conditions_1: ─────────┤ ├┤2 ├──■──┤ ├┤ ├┤ ├»

│ ││ cmp │┌─┴─┐│ c_adder ││ ││ c_adder_dg │»

conditions_2: ─────────┤ ├┤ ├┤ X ├┤0 ├┤ ├┤0 ├»

│ ││ │└───┘│ ││ ││ │»

sum_0: ─────────┤ ├┤ ├─────┤5 ├┤0 ├┤5 ├»

│ ││ │ │ ││ F ││ │»

sum_1: ─────────┤ ├┤ ├─────┤6 ├┤1 ├┤6 ├»

│ ││ │ │ ││ ││ │»

sum_2: ─────────┤ ├┤ ├─────┤7 ├┤2 ├┤7 ├»

│ ││ │ │ ││ ││ │»

work_0: ─────────┤3 ├┤3 ├─────┤8 ├┤4 ├┤8 ├»

└──────┘└──────┘ │ ││ ││ │»

work_1: ──────────────────────────────┤9 ├┤5 ├┤9 ├»

│ ││ ││ │»

work_2: ──────────────────────────────┤10 ├┤6 ├┤10 ├»

└───────────┘└────┘└──────────────┘»

« ┌─────────┐

« state_0: ────────────────┤0 ├

« │ │

« state_1: ────────────────┤1 ├

« ┌─────────┐│ │

« state_2: ─────┤0 ├┤ ├

« │ ││ │

« state_3: ─────┤1 ├┤ ├

« │ ││ │

« obj: ─────┤ ├┤ ├

« │ ││ │

«conditions_0: ──■──┤ ├┤2 ├

« │ │ ││ cmp_dg │

«conditions_1: ──■──┤2 ├┤ ├

« ┌─┴─┐│ cmp_dg ││ │

«conditions_2: ┤ X ├┤ ├┤ ├

« └───┘│ ││ │

« sum_0: ─────┤ ├┤ ├

« │ ││ │

« sum_1: ─────┤ ├┤ ├

« │ ││ │

« sum_2: ─────┤ ├┤ ├

« │ ││ │

« work_0: ─────┤3 ├┤3 ├

« └─────────┘└─────────┘

« work_1: ───────────────────────────

«

« work_2: ───────────────────────────

«

objective qubit index 4

[10]:

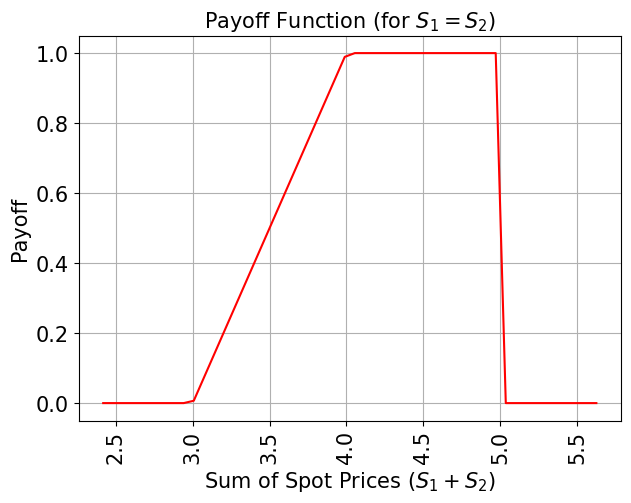

# plot exact payoff function

plt.figure(figsize=(7, 5))

x = np.linspace(sum(low), sum(high))

y = (x <= 5) * np.minimum(np.maximum(0, x - strike_price_1), strike_price_2 - strike_price_1)

plt.plot(x, y, "r-")

plt.grid()

plt.title("Payoff Function (for $S_1 = S_2$)", size=15)

plt.xlabel("Sum of Spot Prices ($S_1 + S_2)$", size=15)

plt.ylabel("Payoff", size=15)

plt.xticks(size=15, rotation=90)

plt.yticks(size=15)

plt.show()

[11]:

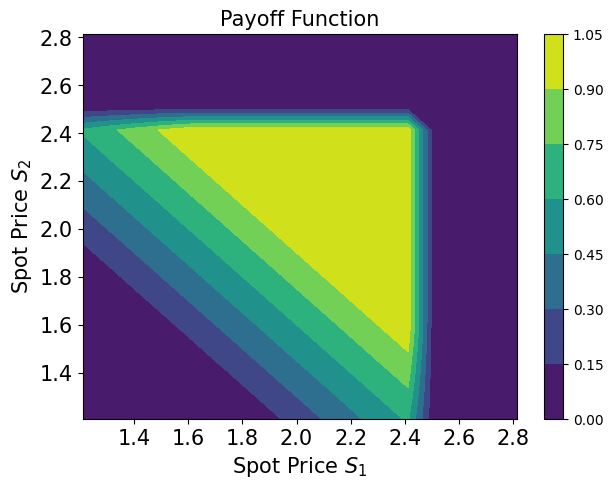

# plot contour of payoff function with respect to both time steps, including barrier

plt.figure(figsize=(7, 5))

z = np.zeros((17, 17))

x = np.linspace(low[0], high[0], 17)

y = np.linspace(low[1], high[1], 17)

for i, x_ in enumerate(x):

for j, y_ in enumerate(y):

z[i, j] = np.minimum(

np.maximum(0, x_ + y_ - strike_price_1), strike_price_2 - strike_price_1

)

if x_ > barrier or y_ > barrier:

z[i, j] = 0

plt.title("Payoff Function", size=15)

plt.contourf(x, y, z)

plt.colorbar()

plt.xlabel("Spot Price $S_1$", size=15)

plt.ylabel("Spot Price $S_2$", size=15)

plt.xticks(size=15)

plt.yticks(size=15)

plt.show()

[12]:

# evaluate exact expected value

sum_values = np.sum(u.values, axis=1)

payoff = np.minimum(np.maximum(sum_values - strike_price_1, 0), strike_price_2 - strike_price_1)

leq_barrier = [np.max(v) <= barrier for v in u.values]

exact_value = np.dot(u.probabilities[leq_barrier], payoff[leq_barrier])

print("exact expected value:\t%.4f" % exact_value)

exact expected value: 0.8023

[13]:

num_state_qubits = asian_barrier_spread.num_qubits - asian_barrier_spread.num_ancillas

print("state qubits: ", num_state_qubits)

transpiled = transpile(asian_barrier_spread, basis_gates=["u", "cx"])

print("circuit width:", transpiled.width())

print("circuit depth:", transpiled.depth())

state qubits: 5

circuit width: 14

circuit depth: 6049

[14]:

asian_barrier_spread_measure = asian_barrier_spread.measure_all(inplace=False)

sampler = Sampler()

job = sampler.run(asian_barrier_spread_measure)

[15]:

# evaluate the result

value = 0

probabilities = job.result().quasi_dists[0].binary_probabilities()

for i, prob in probabilities.items():

if prob > 1e-4 and i[-num_state_qubits:][0] == "1":

value += prob

# map value to original range

mapped_value = objective.post_processing(value) / (2**num_uncertainty_qubits - 1) * (high_ - low_)

print("Exact Operator Value: %.4f" % value)

print("Mapped Operator value: %.4f" % mapped_value)

print("Exact Expected Payoff: %.4f" % exact_value)

Exact Operator Value: 0.6318

Mapped Operator value: 0.8357

Exact Expected Payoff: 0.8023

[16]:

# set target precision and confidence level

epsilon = 0.01

alpha = 0.05

problem = EstimationProblem(

state_preparation=asian_barrier_spread,

objective_qubits=[objective_index],

post_processing=objective.post_processing,

)

# construct amplitude estimation

ae = IterativeAmplitudeEstimation(

epsilon, alpha=alpha, sampler=Sampler(options={"shots": 100, "seed": 75})

)

[17]:

result = ae.estimate(problem)

[18]:

conf_int = (

np.array(result.confidence_interval_processed)

/ (2**num_uncertainty_qubits - 1)

* (high_ - low_)

)

print("Exact value: \t%.4f" % exact_value)

print(

"Estimated value:\t%.4f"

% (result.estimation_processed / (2**num_uncertainty_qubits - 1) * (high_ - low_))

)

print("Confidence interval: \t[%.4f, %.4f]" % tuple(conf_int))

Exact value: 0.8023

Estimated value: 0.8283

Confidence interval: [0.8202, 0.8363]

[ ]: