02-Finance Tutorial-Portfolio Diversification

[1]:

#Reference to this example:

#https://qiskit-community.github.io/qiskit-finance/tutorials/02_portfolio_diversification.html

[2]:

# Import requisite modules

import math

import datetime

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

# Import Qiskit packages

from qiskit.circuit.library import TwoLocal

#from qiskit_aer.primitives import Sampler

from qiskit_algorithms import NumPyMinimumEigensolver, QAOA, SamplingVQE

from qiskit_algorithms.optimizers import COBYLA

from qiskit_optimization.algorithms import MinimumEigenOptimizer

# The data providers of stock-market data

from qiskit_finance.data_providers import RandomDataProvider

from qiskit_finance.applications.optimization import PortfolioDiversification

import QuantumRingsLib

from QuantumRingsLib import QuantumRingsProvider

from quantumrings.toolkit.qiskit import QrBackendV2

provider = QuantumRingsProvider(token =<YOUR_TOKEN>, name=<YOUR_ACCOUNT>)

backend = QrBackendV2(provider)

from quantumrings.toolkit.qiskit import QrSamplerV1 as Sampler

[3]:

# Generate a pairwise time-series similarity matrix

seed = 123

stocks = ["TICKER1", "TICKER2"]

n = len(stocks)

data = RandomDataProvider(

tickers=stocks,

start=datetime.datetime(2016, 1, 1),

end=datetime.datetime(2016, 1, 30),

seed=seed,

)

data.run()

rho = data.get_similarity_matrix()

[4]:

q = 1 # q less or equal than n

[5]:

class ClassicalOptimizer:

def __init__(self, rho, n, q):

self.rho = rho

self.n = n # number of inner variables

self.q = q # number of required selection

def compute_allowed_combinations(self):

f = math.factorial

return int(f(self.n) / f(self.q) / f(self.n - self.q))

def cplex_solution(self):

# refactoring

rho = self.rho

n = self.n

q = self.q

my_obj = list(rho.reshape(1, n**2)[0]) + [0.0 for x in range(0, n)]

my_ub = [1 for x in range(0, n**2 + n)]

my_lb = [0 for x in range(0, n**2 + n)]

my_ctype = "".join(["I" for x in range(0, n**2 + n)])

my_rhs = (

[q]

+ [1 for x in range(0, n)]

+ [0 for x in range(0, n)]

+ [0.1 for x in range(0, n**2)]

)

my_sense = (

"".join(["E" for x in range(0, 1 + n)])

+ "".join(["E" for x in range(0, n)])

+ "".join(["L" for x in range(0, n**2)])

)

try:

my_prob = cplex.Cplex()

self.populatebyrow(my_prob, my_obj, my_ub, my_lb, my_ctype, my_sense, my_rhs)

my_prob.solve()

except CplexError as exc:

print(exc)

return

x = my_prob.solution.get_values()

x = np.array(x)

cost = my_prob.solution.get_objective_value()

return x, cost

def populatebyrow(self, prob, my_obj, my_ub, my_lb, my_ctype, my_sense, my_rhs):

n = self.n

prob.objective.set_sense(prob.objective.sense.minimize)

prob.variables.add(obj=my_obj, lb=my_lb, ub=my_ub, types=my_ctype)

prob.set_log_stream(None)

prob.set_error_stream(None)

prob.set_warning_stream(None)

prob.set_results_stream(None)

rows = []

col = [x for x in range(n**2, n**2 + n)]

coef = [1 for x in range(0, n)]

rows.append([col, coef])

for ii in range(0, n):

col = [x for x in range(0 + n * ii, n + n * ii)]

coef = [1 for x in range(0, n)]

rows.append([col, coef])

for ii in range(0, n):

col = [ii * n + ii, n**2 + ii]

coef = [1, -1]

rows.append([col, coef])

for ii in range(0, n):

for jj in range(0, n):

col = [ii * n + jj, n**2 + jj]

coef = [1, -1]

rows.append([col, coef])

prob.linear_constraints.add(lin_expr=rows, senses=my_sense, rhs=my_rhs)

[6]:

# Instantiate the classical optimizer class

classical_optimizer = ClassicalOptimizer(rho, n, q)

# Compute the number of feasible solutions:

print("Number of feasible combinations= " + str(classical_optimizer.compute_allowed_combinations()))

# Compute the total number of possible combinations (feasible + unfeasible)

print("Total number of combinations= " + str(2 ** (n * (n + 1))))

Number of feasible combinations= 2

Total number of combinations= 64

[7]:

# Visualize the solution

def visualize_solution(xc, yc, x, C, n, K, title_str):

plt.figure()

plt.scatter(xc, yc, s=200)

for i in range(len(xc)):

plt.annotate(i, (xc[i] + 0.015, yc[i]), size=16, color="r")

plt.grid()

for ii in range(n**2, n**2 + n):

if x[ii] > 0:

plt.plot(xc[ii - n**2], yc[ii - n**2], "r*", ms=20)

for ii in range(0, n**2):

if x[ii] > 0:

iy = ii // n

ix = ii % n

plt.plot([xc[ix], xc[iy]], [yc[ix], yc[iy]], "C2")

plt.title(title_str + " cost = " + str(int(C * 100) / 100.0))

plt.show()

[8]:

from qiskit_algorithms.utils import algorithm_globals

class QuantumOptimizer:

def __init__(self, rho, n, q):

self.rho = rho

self.n = n

self.q = q

self.pdf = PortfolioDiversification(similarity_matrix=rho, num_assets=n, num_clusters=q)

self.qp = self.pdf.to_quadratic_program()

# Obtains the least eigenvalue of the Hamiltonian classically

def exact_solution(self):

exact_mes = NumPyMinimumEigensolver()

exact_eigensolver = MinimumEigenOptimizer(exact_mes)

result = exact_eigensolver.solve(self.qp)

return self.decode_result(result)

def sampling_vqe_solution(self):

algorithm_globals.random_seed = 100

cobyla = COBYLA()

cobyla.set_options(maxiter=250)

ry = TwoLocal(n, "ry", "cz", reps=5, entanglement="full")

svqe_mes = SamplingVQE(sampler=Sampler(backend=backend), ansatz=ry, optimizer=cobyla)

svqe = MinimumEigenOptimizer(svqe_mes)

result = svqe.solve(self.qp)

return self.decode_result(result)

def qaoa_solution(self):

algorithm_globals.random_seed = 1234

cobyla = COBYLA()

cobyla.set_options(maxiter=250)

qaoa_mes = QAOA(sampler=Sampler(backend=backend), optimizer=cobyla, reps=3)

qaoa = MinimumEigenOptimizer(qaoa_mes)

result = qaoa.solve(self.qp)

return self.decode_result(result)

def decode_result(self, result, offset=0):

quantum_solution = 1 - (result.x)

ground_level = self.qp.objective.evaluate(result.x)

return quantum_solution, ground_level

[9]:

# Instantiate the quantum optimizer class with parameters:

quantum_optimizer = QuantumOptimizer(rho, n, q)

[10]:

# Check if the binary representation is correct. This requires CPLEX

try:

import cplex

# warnings.filterwarnings('ignore')

quantum_solution, quantum_cost = quantum_optimizer.exact_solution()

print(quantum_solution, quantum_cost)

classical_solution, classical_cost = classical_optimizer.cplex_solution()

print(classical_solution, classical_cost)

if np.abs(quantum_cost - classical_cost) < 0.01:

print("Binary formulation is correct")

else:

print("Error in the formulation of the Hamiltonian")

except Exception as ex:

print(ex)

[0. 1. 0. 1. 0. 1.] 1.000779571614484

[1. 0. 1. 0. 1. 0.] 1.000779571614484

Binary formulation is correct

[11]:

ground_state, ground_level = quantum_optimizer.exact_solution()

print(ground_state)

classical_cost = 1.000779571614484 # obtained from the CPLEX solution

try:

if np.abs(ground_level - classical_cost) < 0.01:

print("Ising Hamiltonian in Z basis is correct")

else:

print("Error in the Ising Hamiltonian formulation")

except Exception as ex:

print(ex)

[0. 1. 0. 1. 0. 1.]

Ising Hamiltonian in Z basis is correct

[12]:

svqe_state, svqe_level = quantum_optimizer.sampling_vqe_solution()

print(svqe_state, svqe_level)

try:

if np.linalg.norm(ground_state - svqe_state) < 0.01:

print("SamplingVQE produces the same solution as the exact eigensolver.")

else:

print(

"SamplingVQE does not produce the same solution as the exact eigensolver, but that is to be expected."

)

except Exception as ex:

print(ex)

[0. 1. 0. 1. 0. 1.] 1.000779571614484

SamplingVQE produces the same solution as the exact eigensolver.

[13]:

xc, yc = data.get_coordinates()

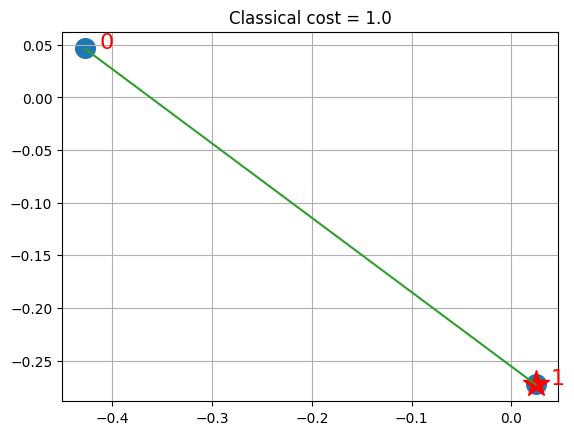

visualize_solution(xc, yc, ground_state, ground_level, n, q, "Classical")

[14]:

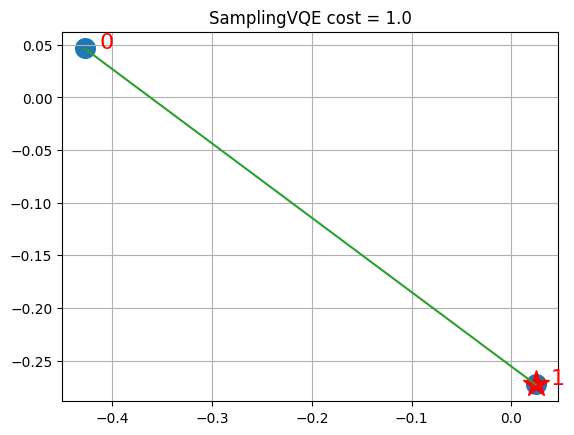

visualize_solution(xc, yc, svqe_state, svqe_level, n, q, "SamplingVQE")

[ ]: